Recover More Revenue from Delinquent Borrowers — Without Increasing Regulatory Risk

Loss Mitigation Infrastructure for Modern Lenders

Robert Purtill, Founder & CEO

Solutions Born From A Decade Inside the Hardest Edge of Consumer Credit

My name's Robert Purtill. Before founding SARYSSA, I was a top performer for over ten years inside consumer debt resolution - where borrowers are distressed, traditional servicing has failed, and regulatory scrutiny is constant.

During that time, I worked directly with tens of thousands of distressed borrowers, navigating hardship, repayment breakdowns, negotiated resolutions, and the compliance constraints of operating in highly regulated financial markets.

That experience offered invaluable insight into why borrowers exit the creditor ecosystem entirely, why hardship programs fail and how inconsistent policies create both financial loss and regulatory risk for creditors.

What became clear is that debt settlement exists as a system failure — not because it’s optimal for lenders or borrowers, but because most creditors lack structured, scalable ways to identify hardship early, offer viable alternatives, and manage resolution consistently.

SARYSSA exists to help lenders reclaim that ground: improving recoveries while strengthening governance, auditability, and customer outcomes.

The Reality of Lending Today

Delinquencies and loss rates are material and rising, with real impact on recoveries and charge-offs.Hardship & workout options for struggling borrowers are limited, manual, and inconsistent - creating exceptions, leakage, and operational friction.Processes are fragmented across agents, spreadsheets, servicers, and third parties, making execution unreliable.Customer awareness of hardship options is low, and lenders struggle to surface offers without creating moral hazard or policy drift.Regulatory pressure is increasing, especially where lenders let clients drift to outside agencies or debt settlement companies.Visibility and measurement are weak - most lenders cannot quickly show which offers were made, accepted, and how they performed.

Our Solution

Offer 1: Manual Pilot

What we do:We review your current methods for handling struggling borrowers, past-due accounts, and non-performing loans.Build and implement optimized playbooks, with rules to create offers and payment plans for struggling borrowersGive agents clear guidance on what they can offer and whenRun a short pilot on one segment of accountsMeasure outcomes vs. your current baselineYou use your existing tech infra:

No heavy IT lift.

No long contracts.The goal: recover more, eliminate operational friction and reduce risk — fast.

Offer 2: SARYSSA SaaS

Manual Pilot → Next-Gen ResolutionOSFor teams that want to turn proven hardship and workout playbooks into durable, auditable infrastructure.

First we implement our manual pilotThen we automate it into software so you can scale it and audit it.This includes:

Clear rules and approval pathsLess exception-driven decision makingTracking of offers and outcomesBetter reporting for compliance and auditsA cleaner experience for agents and borrowersThe goal: a repeatable, optimized system you can trust, not spreadsheets and guesswork.

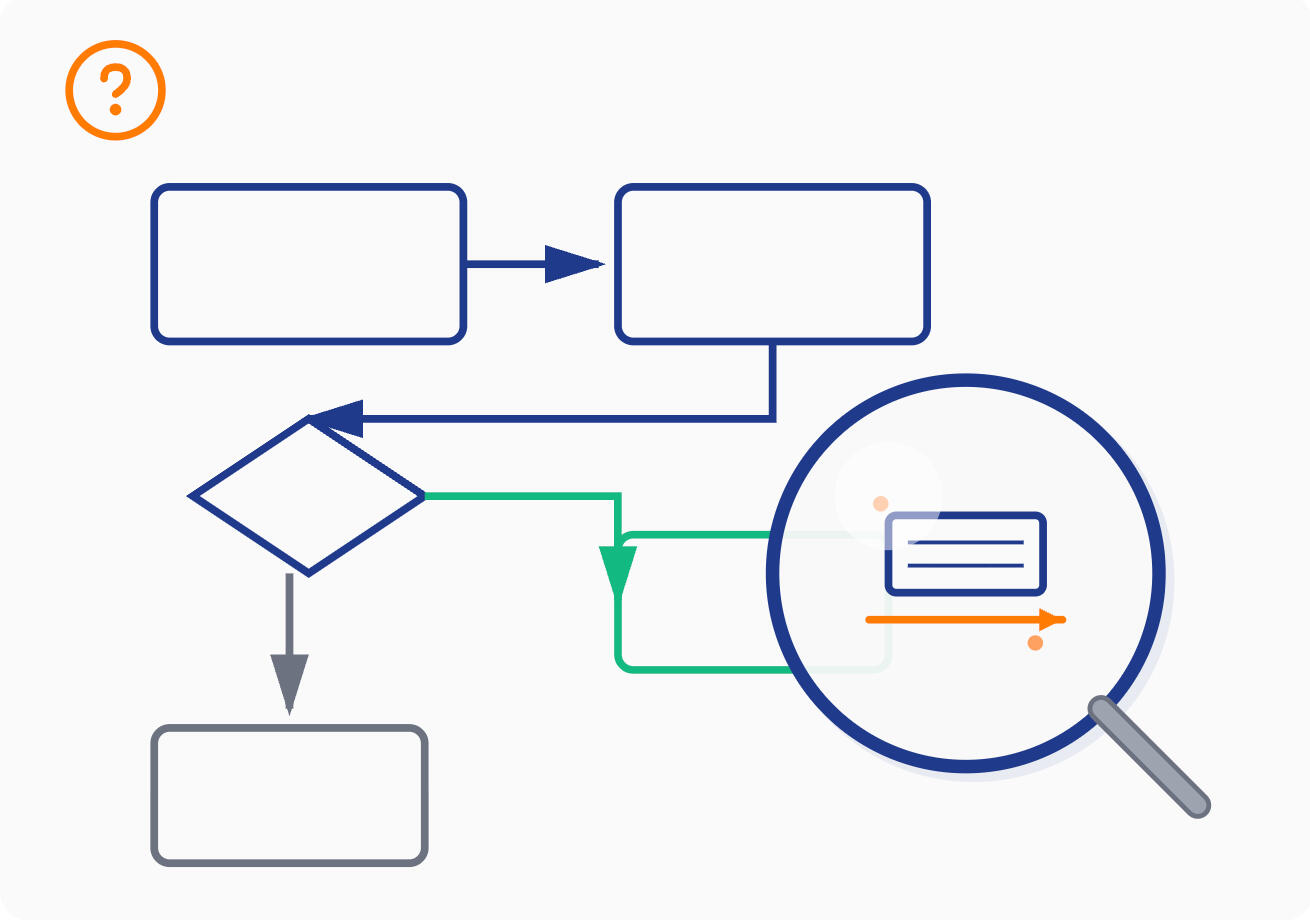

How it Works

1. Discovery & Design

You show us how you handle distressed borrowers and late-stage accounts today. We map your current flow and design a better process.

2. Pilot & Measurement

We run a controlled pilot and show improvement.

3. Platform & Scale

We systematize best practices into a governed, auditable software that enforces the rules and tracks outcomes.

Who We Help

• Consumer lenders• Credit card issuers• Personal loan lenders• Digital lenders and fintechs• BNPL and POS lenders• Non-bank lenders serving U.S. consumers•Servicing and collections teams who want cleaner rules and results

We work best with lenders who want:• Better recoveries• Fewer complaints• Clean compliance posture and reporting for regulators• A clear system instead of ad-hoc decisions

Regulatory-Aligned, Compliance-Ready by Design

Lenders are under increased scrutiny for how they treat distressed borrowers. Manual exceptions, opaque decisions, and weak reporting expose the organization. Our approach structures hardship and workout decisions so they are consistent, documented, and fully explainable to examiners.

What We're Hearing from Lenders

“We can’t explain to auditors why certain workout decisions were made—too many one-off exceptions.”“Hardship flows live in spreadsheets and email. We can’t track who was offered what or how plans perform.”“IT can’t push policy changes quickly. Everything takes months.”“Agents know the rules, but they still freelance. We lack consistency.”

Do we need to integrate with core systems to start?

A: No. Early pilots run manually or semi-manually using your existing systems, with light data pulls. Integration only becomes relevant once a repeatable workflow is proven.

How is data handled and controlled?

A: Pilots are scoped to small segments and operate inside your compliance framework. Access is permissioned, activity is logged, and outputs support audit review.

What if we already have hardship workout policies?

A: Most lenders do. The recurring problem is consistency and execution: exceptions, undocumented overrides, and poor visibility. The pilot strengthens execution and measurement—not just policy wording.

What if performance doesn’t improve?

A: Pilots are scoped, short-cycle, and reversible. If the program fails to demonstrate clear value, you stop. You aren’t locked into long-term platform commitments before evidence.

Schedule Your Discovery Call Now

In 30 minutes, we'll discuss your current challenges, portfolio metrics, and how SARYSSA can deliver measurable ROI.✓No sales pitch—just an honest assessment of fit

✓Walk through your specific use cases

✓Get a custom ROI estimate for your portfolio

© SARYSSA. All rights reserved.

Thanks!

Tempor purus penatibus neque laoreet auctor fusce imperdiet accumsan etiam vis lacus sodales arcu luctus sodales cursus curae vel vestibulum non dolor faucibus.